As addressed in the prior article, geocoded results with high accuracy and precision are important to property insurers, allowing for the identification, analysis, and pricing of risk. In turn, accurate pricing of risk is beneficial to insurance consumers. Knowing the risk—and the cost to insure it—can help current and prospective homeowners make more informed decisions. Accurate risk pricing can even lead to more resilient communities, as mitigation investments can be allocated more efficiently.

Why is spatial resolution important in risk pricing?

Spatial resolution refers to the type and granularity of location data for a single parcel and how it is represented geographically. There are four different levels of spatial resolution that are possible within property parcel data: parcel centroid, delivery point, building centroid, and building footprints. See the sidebar for more on common geocoding results scenarios. The distinction between these options is important because of the implications tied to each and how they represent an insured structure. In the case of the last three, there could be multiple units and/or structures on the same parcel, resulting in more than one result per parcel. This complexity is relevant to understanding how structures interact with risk.

What is spatial resolution in geocoding?

In the context of address geocoding for property insurance, spatial resolution refers to the level of detail and precision at which a given property or building can be identified and represented geographically. Determining the precision needed for a geocoded point location depends on the use case. The highest level of detail—or spatial resolution—is not always necessary for property insurance applications. There are certain use cases, such as wind and hail risk, where less granular spatial resolution is sufficient for ratemaking. However, in certain applications, understanding the exact location of a property is essential to insurance pricing because risk can be driven by highly localized conditions. For instance, for property insurance perils like flood and wildfire, it can be important to know an insured building’s exact location. However, this is not always the point returned by the standard geocoding process.

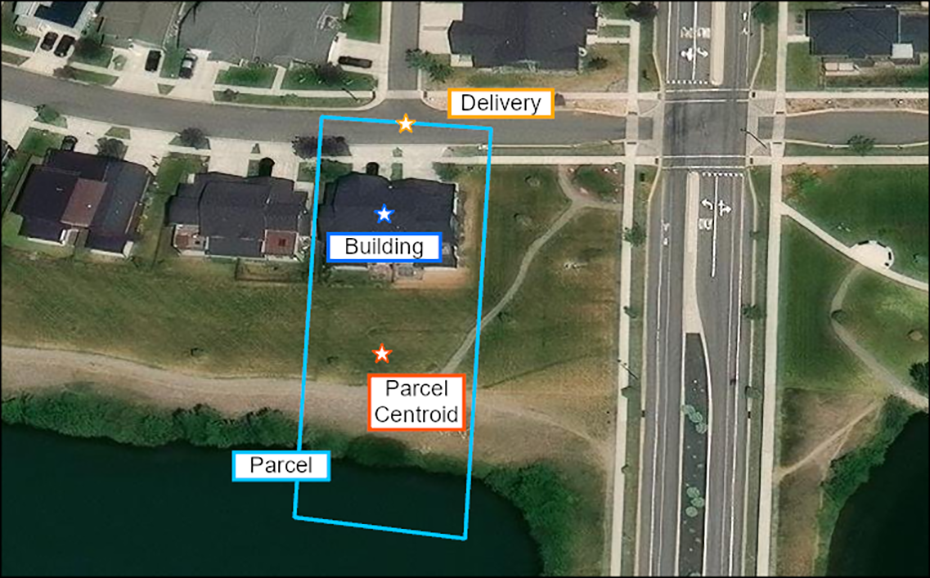

Figure 1: Schematic showing several possible levels of spatial resolution and corresponding geographic representation when considering a single parcel

Source: Milliman analysis using Esri ArcGIS Online data and maps. Base map service layer credits: Esri, Maxar, Microsoft.

Imagine a scenario where, on a given parcel of land, a home sits up a steep slope from a river. The geocoder may assign the located point to the center of a parcel, regardless of the location of the home on the property. However, where the home sits in relation to the river can impact its risk of flooding. If there is even a slight difference in elevation between the located point and the building itself, that small change can result in a significantly different assessment of flood risk. In turn, this can lead to a significantly different flood premium.

To improve pricing accuracy, the geocoders can be supplemented by data describing the extent of the insured structure, or a building footprint. By either requiring the geocoded point to fall within the building (known as a rooftop match) or by using the footprint itself as the recorded spatial data, the accuracy of the geocoding process is increased, and risk can be assessed more carefully.

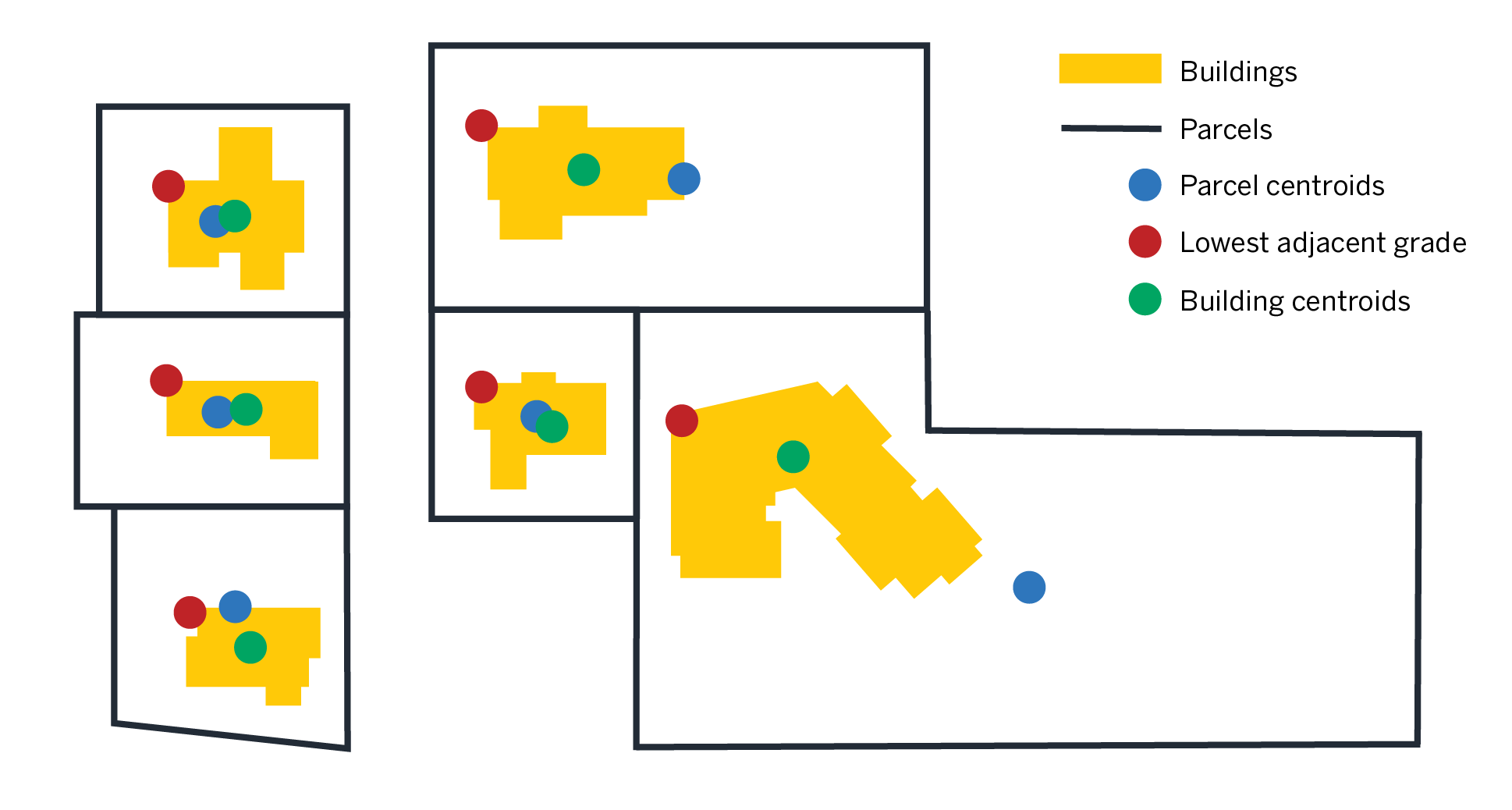

Figure 2: Schematic showing how building footprints can provide a more accurate analysis of risk by defining the extent of an insured structure

How can building footprints be used in geocoding?

Building footprints are spatial data elements that represent insured structures, such as homes, offices, or other buildings, and can be integrated into the geocoding process to increase location accuracy. In addition to increased accuracy, building footprints can improve identification of detached structures on both residential and commercial properties. Given the larger parcel sizes and multiple facilities at a single address, building footprints should be particularly attractive to commercial property insurers, but carriers and their vendors may not be able to process this data type using existing workflows. However, there are ways to customize workflows to accommodate multiple types of spatial data. The flexibility of building footprint data comes from the ability to include multiple levels of spatial resolution while considering the entire structure. For example, when underwriting flood risk, insurers might consider the elevation of the lowest adjacent grade (LAG) along the perimeter of the foundation or the area of a building at risk of flooding in different events. These adaptive techniques can result in better risk quantification compared to a single geocoded point.

Why geocoding can make a difference in insurance: A use case

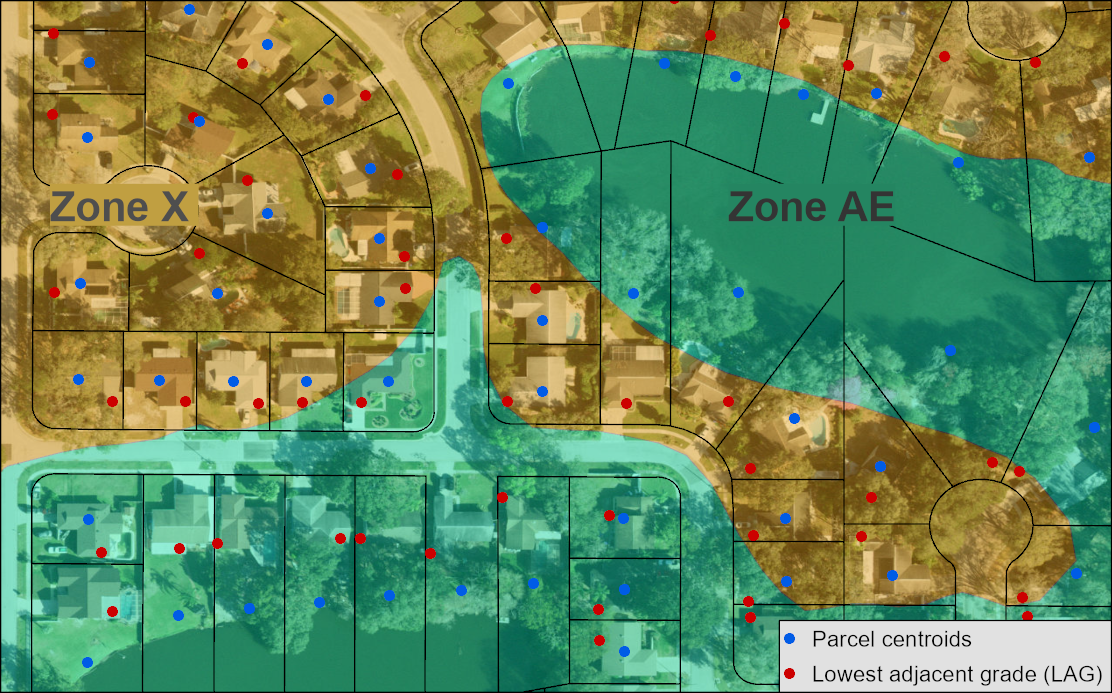

The accuracy of the geocoded location can translate to how well the insurance premium accounts for risk. For flood insurance applications, two critical risk drivers are a building’s distance to water and elevation. Examine the scenario in Figure 3.

Figure 3: Parcels showing dislocation between the determined parcel centroid vs. the insured building’s lag

Source: Milliman analysis using the FEMA National Flood Hazard Layer and Florida Geographic Information Office statewide parcel data. Base map service layer credits: Esri, Microsoft, Vantor.

Note: Depending on the location of the insured structure, the difference in rating the two locations within one parcel could be significant.

In Figure 3, blue dots represent the parcel centroids, while red dots represent the LAG derived from vertices of building footprints considered in the geocoding process. At times, the parcel centroids lie in different risk zones than the LAGs. Additionally, the two locations may vary up to several meters in elevation. Although this spatial dislocation may seem insignificant, the risk modeled for each of the two points is distinct. This example illustrates how seemingly small changes can significantly increase or decrease insurance premiums.

Key takeaways

The benefit of using building footprints for geocoding is twofold: providing the maximum amount of information relative to an insured structure and maximizing the accuracy of geographic variables. Instead of an arbitrary point, which possibly hits the building, the geometry of the structure is considered. For insurers and managing general agents (MGAs) that are determining pricing for highly location dependent risks, adopting geocoding processes that can include multiple levels of spatial resolution can lead to more accurate risk quantification.